Required Minimum Distributions (RMDs)

Required Minimum Distributions (RMDs)

Rules, Deadlines, and Tax Strategies for Retirees

If you have a tax-deferred retirement account, the IRS will eventually require you to begin taking withdrawals. These mandatory withdrawals are called Required Minimum Distributions or RMDs.

If you turn 73 or older this year understanding the rules and deadlines for RMDs is critical. Missing a deadline or miscalculating the amount can lead to unnecessary taxes and penalties.

What is an RMD?

An RMD is the minimum amount the IRS requires you to withdraw annually from certain retirement accounts after reaching age 73. This mandatory distribution applies to traditional IRAs, 401(k)s, 403(b)s, and 457 plans, SEPs and SIMPLE IRAs.

Roth IRAs are exempt from RMD requirements during the owner’s lifetime.

When do RMDs Begin?

Under the Secure Act 2.0, your first RMD must be withdrawn by April 1 of the year following your 73rd birthday. For example, if you turn 73 on February 2, 2026, you must take your first RMD by April 1, 2027. Every year after that the RMD must be taken by December 31.

Be careful if you delay your first RMD until the April 1st deadline as you will have to take two taxable distributions that year. You will take one RMD for your 73rd birthday by April 1st and one for your 74th birthday by December 31 of same year. Depending upon the size of your IRA, this could bump you up to a higher tax bracket, so consider the tax impact carefully. You should consult a tax professional for advice.

How are RMDs Calculated?

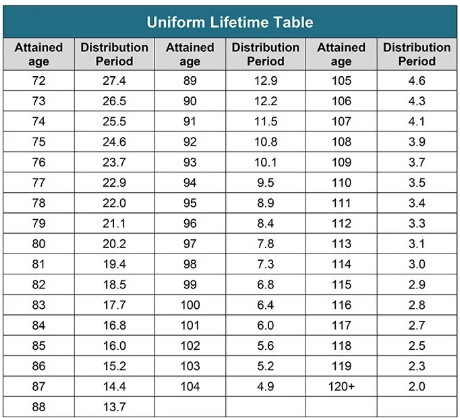

You start with the account balance of your IRA on December 31 of the previous year. So, for 2026 RMDs you would start with the account balance on December 31 of 2025. Then you divide that amount by a life expectancy factor provided by the IRS on the Uniform Lifetime Table. You find your age on the table and use the accompanying factor. There are a few exceptions, but most people use the Uniform Lifetime Table. The older you are the higher your annual distribution requirement.

{kind=link}

Your financial advisor or the IRA custodian can help you calculate the exact RMD amount. Ensuring you take the right amount is essential to avoiding unnecessary and costly penalties.

What if you Miss an RMD?

Based on the Secure Act 2.0, the penalty for missing an RMD is 25% of the amount you should have withdrawn plus you need to withdraw the RMD amount you failed to take. This penalty can be reduced to 10% if the error is caught and corrected in a timely manner. Obviously, the best practice is to plan ahead and take your RMDs on time.

How do you Take your RMD?

You have several options:

- You may withdraw your RMD in a lump sum at any time during the year.

- You may choose to take partial distributions throughout the year and even set up an automatic monthly or quarterly distribution directly to your bank account.

- You do not have to take cash. Some retirees opt to transfer shares of stock or mutual funds to a taxable account and keep it invested. This is called an in-kind distribution.

- If you have more than one traditional IRA, you are allowed to aggregate the distributions and take them from one IRA or spread it across multiple IRAs.

- Employer-sponsored plans like 401(k)s must be calculated separately and withdrawn from each 401(k). 401(k) distributions cannot be aggregated.

- The amount of the RMD is reported to you on a form 1099 and taxed as ordinary income in the year withdrawn. This includes any in-kind distributions as well as cash.

A Special Rule for Workplace Plans

If you are still working at age 73 you may be allowed to waive RMDs for the 401(k)-plan associated with your current employer, as long as you do not own 5% or more of the company. The employer plan must include the “still working” provision. Most plans do but confirming this is important.

This waiver does not apply to IRAs, SEPs, SIMPLEs or 401(k)s at former employers. You must take these RMDs on time even if you continue to work.

This special rule allows for some tax planning when you have multiple retirement accounts so it would be wise to consult with a tax professional.

When is the Best Time to Take my RMDs?

The answer to this question depends on your income needs and investment strategy. The tax will be the same whether you take the money in installments throughout the year or in a lump sum at the end of the year.

Some retirees prefer to keep the money invested and let it grow as long as possible, so they take the distribution near the end of the year. If your RMD is part of your regular income plan you probably will want to take monthly distributions throughout the year. As long as you comply with the deadline, the choice of when to take your distributions is up to you.

What Strategies Could Reduce the Impact of RMDs on my Taxable Income?

Large IRAs can be burdensome when it comes to taxes, especially if you do not need the income. It takes proper planning in the years leading up to age 73 to reduce your RMD and the erosion caused by income taxes.

Some basic strategies to reduce RMDs include:

- Qualified Charitable Distributions (QCDs): After age 70.5 taxpayers can donate up to $111,000 per taxpayer in 2026 directly from your IRA to qualified charities. The amount you donate counts toward your RMD and it is not included in your taxable income when properly reported on your income tax return. The maximum allowable is adjusted annually for inflation. This is a valuable tax strategy for all taxpayers, but for those who regularly support charities it can be especially effective to reduce taxes.

- Partial Roth Conversions: Carefully planned Roth IRA conversions spread out annually over several years leading up to age 73 will lower the size of your IRA and reduce future RMDs. Taxes are due in the year of the Roth conversion, but this strategy potentially lowers your lifetime tax liability.

- Voluntary income withdrawals before age 73: Depending upon when you retire, you may have a few lower income tax years before RMDs and Social Security Benefits kick in. You could take some distributions from your IRA to fill a lower tax bracket. If you spread your tax liability over more years you could prevent a large RMD from pushing you into a higher tax bracket later. You have to pay tax on the amount of the Roth conversion in the year withdrawn, but this strategy may lower your lifetime tax liability.

- Coordinate Distributions from your IRA with other Income Sources: Plan your retirement income and take IRA distributions in years when your taxable income is lower. For example, this could mean delaying the start of Social Security benefits and using IRA distributions as income in those early retirement years.

If any of these strategies have piqued your interest and you would like to learn more, be sure to visit How to Reduce Future RMDs: 5 Tax-Efficient Strategies for Retirees.

What is the Biggest RMD Mistake?

Failing to plan is planning to fail. If you wait until the last minute to take your RMD, you miss the opportunity to coordinate it with other income sources for maximum tax efficiency. Like in sports, the goal is to avoid unforced errors. Waiting until the last minute increases the risk of miscalculating your withdrawal amount. Taking too much, results in more taxes than necessary. Taking too little results in unnecessary penalties.

Take time to plan ahead and avoid the unnecessary RMD mistakes.

RMD Planning for Virginia Retirees

Required minimum distributions are only one piece of a retirement income strategy. Many retirees in the Roanoke Valley coordinate RMDs with the decision on when to start Social Security benefits, Roth conversion strategies, charitable giving and estate planning. When you coordinate your RMDs with other income sources, you could achieve a more tax efficient retirement income strategy.

At Guelich Capital Management we work with retirees throughout Virginia to help manage retirement income and navigate the changing tax landscape. Give us a call today to get answers to your questions and start a tax efficient retirement income plan. 540-772-4545. info@guelichcapital.com

This article is for educational purposes only. It should not be considered tax, investment or legal advice. Consult a qualified professional regarding your own specific situation.

Written by Connie C. Guelich, CFP® this article represents our views at the time written, and it is subject to change.